What is bad debt group 3?

Bad debt group 3 is a common term in the credit industry, used to refer to loans that are 30 to 90 days past due and show signs of non-payment on time. When a loan is transferred to group 3 debt, the bank or financial institution will start to monitor closely and take measures to check to ensure the customer's ability to pay.

Bad debt group 3 not as serious as group 4 or 5 debt, but it also shows that customers have begun to have difficulty paying their loans. Understanding the bad debt group 3 help individuals and businesses have a clearer view of their financial status and take timely measures to avoid falling into more serious bad debt groups.

Basic concept of bad debt group 3

When you do not pay your loans within 30 to 90 days, your loan will be transferred to bad debt group 3. During this period, the bank's ability to recover debt is still quite high, however, you still need to take payment measures to avoid making the situation worse. If you do not resolve group 3 debt, you will be at risk of being transferred to group 4 debt or group 5 debt, this will make your financial situation more difficult.

What is group 3 debt?

Group 3 debt These are loans that are 30 to 90 days past due. These loans can be classified as subprime, meaning that there are no signs of loss of capital but the ability to collect the debt is starting to have difficulties. This means that the customer has not paid the debt on time, but is still able to repay and the bank can continue to work with the customer to resolve the loan.

In the bank credit system, group 3 debt be considered doubtful debt. This does not mean that you are completely unable to pay your debts, but the bank needs to monitor closely and ask customers to explain their financial status to avoid risks. Group 3 debt can appear in the following cases:

- Late paying customers: A loan can be transferred group 3 debt when a customer does not pay within 30 to 90 days, but is not yet at risk of losing capital.

- Customers in financial difficulty: Borrowers may experience temporary financial problems that prevent them from making payments on time but may still be able to pay if given more time.

- Change in business situation: A business may have difficulty maintaining cash flow, causing delays in debt payments, but this is not a sign of an uncollectible debt.

Understand group 3 debt to avoid and overcome

Characteristics of group 3 debt

- Overdue payment: Loans in group 3 debt are usually 30 to 90 days overdue and the bank will have to follow up and ask the customer to provide additional information to ensure collectability.

- High risk but still recoverable: Although loans in this group have a higher level of risk, the bank can still recover the debt if the customer makes timely payments in the future.

When will group 3 bad debt be cleared?

When will group 3 bad debt be cleared? is a question of interest to many borrowers, especially those who have overdue loans but have not yet turned into more serious bad debt. According to the regulations of the State Bank of Vietnam, a bad debt, including group 3 debt, will be erase or remove from the credit history when the borrower completes the full payment of the debt and related fees. However, the process of clearing group 3 bad debt is not an automatic process and requires the following conditions:

Conditions for clearing bad debt group 3

- Full payment of debt: The customer must pay the entire loan, including interest and fees. After payment is completed, the bank will consider removing the bad debt status of group 3.

- Payment phase: For overdue loans, if the customer continues to pay on time and does not have any additional overdue debts within 6 months to 1 year, the bank will re-evaluate and may clear group 3 bad debt.

- Bank processing: Banks will review and confirm the completion of loan payments before making a decision to write off bad debt. This may take some time, as the bank needs to conduct checks and update information into the credit system.

Understand the conditions to clear bad debt group 3 if you accidentally get caught

What impact does clearing group 3 bad debt have on credit?

When bad debt group 3 cleared, the customer's credit score will improve. However, it should be noted that clearing group 3 bad debt does not mean that the customer will immediately have a credit score like before. Banks and credit institutions will need time to update information and re-evaluate the customer's credit profile.

Which banks can lend to group 3 bad debt?

Another question that many people with bad debt group 3 are interested in is Which banks can I borrow from if I have bad debt group 3?? When you have bad debt group 3, the ability to borrow capital from large banks will be very difficult. However, some banks and financial institutions have special loan products for people with bad debt group 3.

Banks lend to customers with bad debt group 3

- State Bank: State-owned banks such as Vietcombank, BIDV, Agribank, or VietinBank often have stricter policies when granting credit to customers with bad debts. However, if you can prove your ability to pay in the future or have collateral, you still have the opportunity to borrow capital.

- Private banks: Some private banks or foreign banks have more flexible credit programs and are willing to lend at higher interest rates. Banks such as Sacombank, Techcombank, TPBank also have loan products specifically for customers with bad debt group 3.

- Financial institutions and consumer lending companies: In addition to banks, many financial institutions and consumer lending companies also provide loans to customers with bad debt group 3. However, the interest rates of these organizations are often much higher and require collateral or a guarantor.

Be careful when borrowing capital from banks if you have bad debt group 3

- High interest rate: Banks or financial institutions will apply higher interest rates to customers with bad debt group 3.

- Property security requirements: Banks may require customers to provide collateral or guarantors to minimize risk.

- More stringent loan process: The loan approval process will be more difficult and may require customers to demonstrate their ability to repay debt in the future.

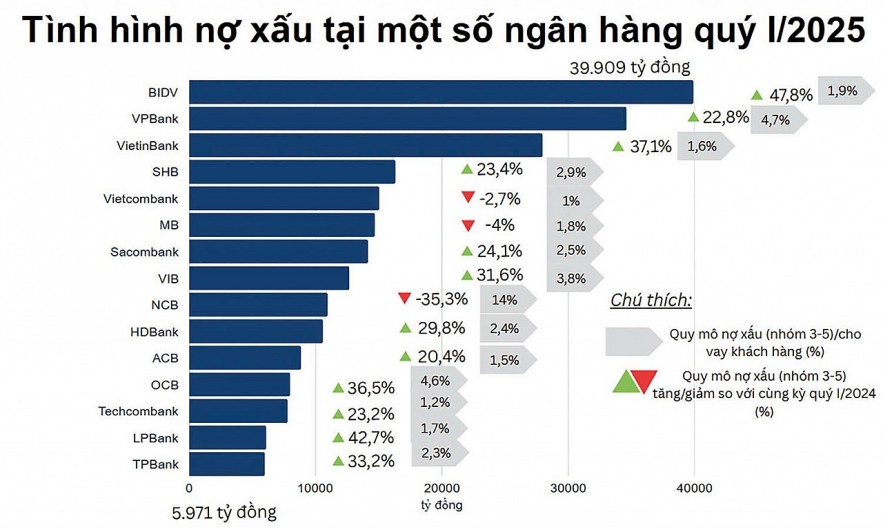

Bad debt situation at some banks in the first quarter of 2025

How to manage and prevent bad debt group 3

To avoid falling into bad debt group 3 and other bad debt groups, you need to have a clear financial management strategy and take effective risk prevention measures.

1. Maintain financial stability

- Individual: Make sure you have a solid financial plan and keep track of your spending. If you have a loan, make a clear repayment plan to avoid overdue payments.

- Business: Ensure that the business has enough cash flow to repay loans on time. This helps maintain creditworthiness and avoid falling into bad debt.

2. Monitor your credit status and credit reports

Individuals and businesses: Periodically check credit reports and monitor loans to promptly handle when detecting signs of overdue debt.

3. Use financial management support tools

Use Livetrade Pro will help you track and manage your loans and credit status effectively. This tool not only helps you control your spending but also provides appropriate financial strategies to avoid falling into bad debt.

In shortWhat is bad debt group 3? and When will group 3 bad debt be cleared?? Loans that are 30 to 90 days overdue are group 3 debt can have a major impact on your ability to borrow money in the future. Understanding the characteristics of group 3 debt and taking timely action will help you improve your financial situation and protect your credit score.

If you are struggling with group 3 bad debt, do not hesitate to seek support from banks or financial institutions, and use tools such as Livetrade Pro to optimize your financial strategy. Download Livetrade Pro now to optimize your financial strategy and manage your personal finances smarter. Start today to manage your finances and protect your future assets.