What is group 1 2 3 4 5 debt?

In the field of credit, the classification of loans into debt group 1, 2, 3, 4, 5 is a method that helps banks and financial institutions assess the risk level of each loan. Each debt group reflects the customer's payment status, thereby helping financial institutions better understand the ability to collect debts. This classification not only helps banks minimize risks but also helps borrowers, whether individuals or businesses, have a clearer view of their financial status.

Classifying debt into groups helps banks accurately assess the credit status of each customer, thereby making decisions on credit granting, loan limits and debt handling measures. Understanding debt groups also helps customers, both individuals and businesses, know the status of their loans and take measures to improve when necessary.

Understanding debt groups in credit loans

Debt groups in banks

The five-group classification of debt is a standard method used by banks to assess the safety of loans. These groups are not only based on the time of overdue, but also reflect the customer's ability to pay. Here is the classification and meaning of each debt group:

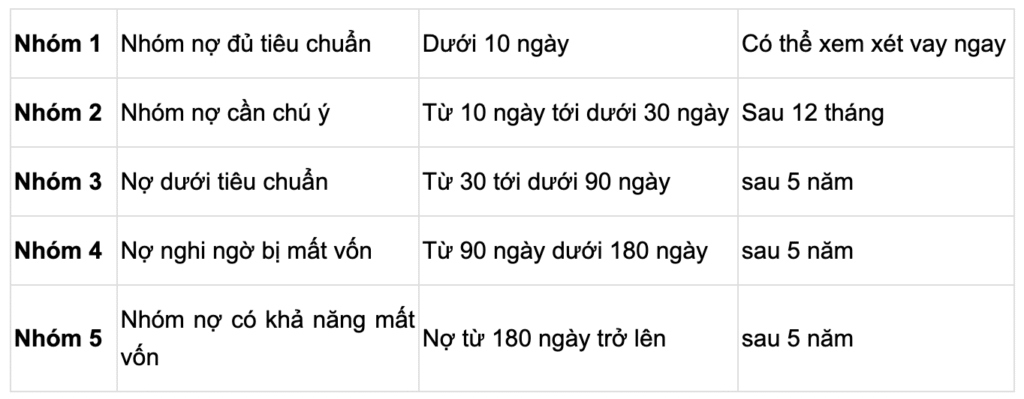

1. Group 1 debt: Standard debt (Safe debt)

Group 1 debt are loans that customers pay on time and show no signs of violating credit conditions. This is a safe debt group and the bank is completely confident about the ability to recover the debt.

- Characteristic: The loan is not overdue, the customer fulfills financial obligations on time and shows no signs of late payment.

- Benefit: Customers in this group will enjoy low interest rates, easier and more favorable loan conditions because the bank does not face great risks in debt collection.

For example: A business borrows from a bank to expand its production activities and makes payments on time. This is a safe loan and will be classified as group 1 debt.

2. Group 2 debt: Debt requiring attention (Substandard debt)

Group 2 debt These are loans that are showing signs of being late or may be delayed but not to the extent that they pose a major risk. These loans are starting to show signs of being late but are not yet too serious.

- Characteristic: Loans are overdue from 1 to 30 days. The customer has not paid on time, however, the ability to repay the debt is still possible.

- Benefit: The bank will monitor these loans closely and require customers to explain the reasons for late payments.

For example: An individual takes out a consumer loan, experiences temporary financial difficulties and is 15 days late in making payments. This loan would be classified as group 2 debt.

3. Group 3 debt: Substandard debt (Doubtful debt)

Group 3 debt are loans that are 30 to 90 days overdue. This is a higher risk debt group, the bank will begin to doubt the customer's ability to recover the debt.

- Characteristic: Loans that are 30 to 90 days overdue have lower payment capacity and the bank will need to take measures to monitor and require the customer to provide financial guarantees.

- Benefit: The bank needs to take debt collection measures, possibly requiring collateral or applying stronger measures.

For example: If a business borrows money and cannot pay after 45 days, this loan will be classified as group 3 debtThe bank will ask the business to explain its financial situation.

4. Group 4 debt: Bad debt

Group 4 debt are loans that are 90 to 180 days overdue. This is a high-risk debt group and the bank will face the possibility of not being able to recover the loan.

- Characteristic: Loans that are 90 to 180 days overdue have a very low chance of recovery and the bank may have to take more aggressive debt collection measures.

- BenefitBanks will need to set aside risk provisions, consider debt collection measures or extend debt to limit losses.

For example: An individual borrows money to invest in a project and fails to repay after 120 days. The loan will be transferred to group 4 debt, the bank will have to take debt collection measures.

5. Group 5 debt: Debt with potential loss of capital (High bad debt)

Group 5 debt are loans that are at risk of being irrecoverable and are overdue for more than 180 days. This is the group of debts with the highest risk level and banks must set aside risk provisions.

- Characteristic: Loans overdue for more than 180 days have a very low chance of recovery and will be transferred by the bank to losses in the financial statements.

- Benefit:These loans are almost impossible to recover and the bank will have to accept the loss.

For example: A business is no longer able to pay its loan after 6 months and is unable to contact its customers. This loan will be transferred to group 5 debt and banks will have to set aside large risk provisions.

Points to note in each debt group

Bad debt group 1 2 3 4 5 and impact on credit

Bad debt group 1 2 3 4 5 are loans that are not paid on time and have the potential to seriously affect the customer's credit history. Classifying bad debts helps banks and credit institutions assess the level of risk and thereby propose debt recovery measures.

Impact of bad debt on individuals:

When an individual has bad credit, their credit history will be severely affected. This reduces their ability to borrow money in the future, as well as increases the cost of borrowing due to higher interest rates. Individuals with bad credit will have difficulty getting loans to buy a house, a car, or a consumer loan.

Impact of bad debt on businesses:

Businesses with bad debts will have difficulty raising capital from banks and credit institutions. When banks assess a business as having many bad debts, they will require larger collateral or refuse to grant credit. This increases the cost of borrowing and limits the business's ability to expand.

Need to understand the effects of bad debt on individuals

How to prevent and manage bad debt

Understand debt groups, especially debt group 1 2 3 4 5 and bad debt group 1 2 3 4 5, will help you have the right financial strategy to avoid falling into bad debt and manage finances effectively.

Maintain good credit history:

- For individuals: Make sure you pay your loans on time to maintain a good credit history and avoid falling into bad debt.

- For business: Ensure that business debts are always paid on time, avoiding overdue situations and affecting the ability to borrow capital.

Track loans and spending:

- For individuals: Keep track of your loans and expenses, especially when you have long-term loans such as home loans and consumer loans.

- For business: Manage cash flow well, ensuring that debts do not exceed repayment capacity. Carefully calculate financial costs and ensure loans are paid on time.

Make a clear financial plan:

- For individuals: Make a personal financial plan to save and invest, ensuring that you are always able to repay your loans on time.

- For business: Long-term financial planning, adjusting business strategies to minimize bad debt and create a strong financial foundation.

Debt group 1 2 3 4 5 is an important part of the credit system and helps banks and financial institutions assess the risk level of loans. Understanding debt groups helps individuals and businesses maintain a clean credit history, thereby easily accessing financial products with favorable conditions.

If you want to optimize your personal or business financial strategy, use Livetrade Pro, a powerful tool to track credit fluctuations and develop effective financial strategies. Download Livetrade Pro now to optimize your financial strategy and manage your personal finances smarter.